Looking at the three hour long video of the event, there is a lot to cover. All of it strikes an uncanny resemblance to a Multilevel Marketing event:

We have a lot of pomp, a lot of hype, bragging, talking about how everyone is forming a giant "family" and asking them to start buying and peddling the newest product - merchant applications. There is a lot of small pieces of information here and there on how they envision their system working, and a lot of it raises red flags.

The event certainly packed a lot of showmanship - live musical performances, important sounding speakers and so on. I've been to a few cryptocurrency conferences already, and they are completely different - you hear a lot about the technology, new developments, etc., and there is a lot less cult of personality.

Merchant program

One of the more important but overlooked parts of the event was the news about OneCoin's new merchant program. There are two new packages being sold - one for $1000 that comes with one whitelabel application, and a $5500 one that comes with seven applications. OneCoin expects its members to purchase those applications and sign up merchants, giving them those applications. Their goal is to reach one million merchants in the coming years. With the merchant adoption, the coin is supposed to gain liquidity and value.

Why should the merchants join? To gain access to OneCoin's "family" and the network, and they incur no cost for the first year. The coin should be "very stable" and merchants "should prefer it to PayPal, Visa, Mastercard".

So yes, the merchant program is as they say "free", and by free, they mean it costs $1000 to the person that signs up the merchant. So the marketing and on-boarding the merchants falls on the coin users that also get to pay for the privilege. But at least you will finally have some place to spend your OneCoins, right?

Well, not quite. The merchants will be able to specify how many OneCoins they will be accepting. They can choose to accept, say, 20% of the payment in OneCoin and 80% from the user's Credit Card (conveniently connected to the account already). This implies that OneCoin doesn't even do the most basic thing that every Bitcoin payment processor does - sell the coins for the merchant and pay them in fiat.

So let's compare that to say, BitPay, one of Bitcoin's oldest payment processors. It allows you to sign up for free, it's free to use for some small volume transactions, or it costs the merchant 1% otherwise. You can accept Bitcoin for 100% of the purchase and you get all of your money in whatever form you want - BTC, wire, etc. For OneCoin, you need to have someone else pay $1000 for the application, sign you up, then you specify how much OneCoins you will be accepting for every transaction, then you have to figure out how to cash those out (without a real exchange yet), and you might be charged something after a year of using it.

So yeah, it doesn't look good - more like a barely serviceable product that you want your current members to buy and convince people to use to make their coin accepted somewhere and thus gain value. It's a good MLM strategy, but terrible usability strategy.

Other things

We've already covered the coin doubling event, so there isn't much more to cover in that regard. It's silly, watching people get excited for a 100% increase in coin supply without an increase in coin's value. So instead, here is a list of various pieces of information that were stated thorough the event:

There have been 14 million accounts created, with 2.5M active distributors

The price of the coin was 50 eurocents, now it is 9 euros, and they aim to get to 25 euros

OneCoin is launching some social media website called OneSaito, which will feature Groupon-like discounts. So it's like 2010

"To make sure we continue to produce coins, we need tokens, and tokens come from product packages"

They want to achieve critical mass in a year's time

"We will eventually move to the next stage when what we're doing will become self-evident" - do they mean people will catch on to the MLM structure?

"We don't want to create idiots"

"Any one of you could've launched Pokemon Go"

Whoever maxes out their 35k Euro contribution on the day of the event will have the opportunity to max out another 35k Euro contribution the following day

OneCoin is a special network, because it acts "like a family"

Conclusions

OneCoin is quite obviously a MLM pyramid scheme. Quite brilliant actually - instead of peddling products people have to start storing in their garages and try to sell to other people, they are selling a "crypto" currency and telling everyone to buy as much as they can to raise it's value. They have virtually no production costs, therefore every dollar spend is essentially profit. Instead of investing that money into development of some actual products, like exchanges, payment processors, etc., they just get people to buy into the scheme more and more, to promote the coin further to drive the sales.

The most symbolic part of the event came in around 2:35. The speakers talk about celebrating OneCoin's second birthday with a cake, "the largest cake ever" - OneCoinCake. 2x2 meters in diameter. Unfortunately, since there were 11500 people in the audience during the event, "not everyone will get to taste the cake". This is perhaps a good analogy to how OneCoin works - everyone pays for the cake, you make a large cake, and the elites will stuff themselves while everyone else will only get to admire the cake from afar...

"Biggest coin out there is Ripplecoin [sic], with 100 billion coins[sic]", and OneCoin will increase its number of coins to 120 Billion to be bigger than Ripple.

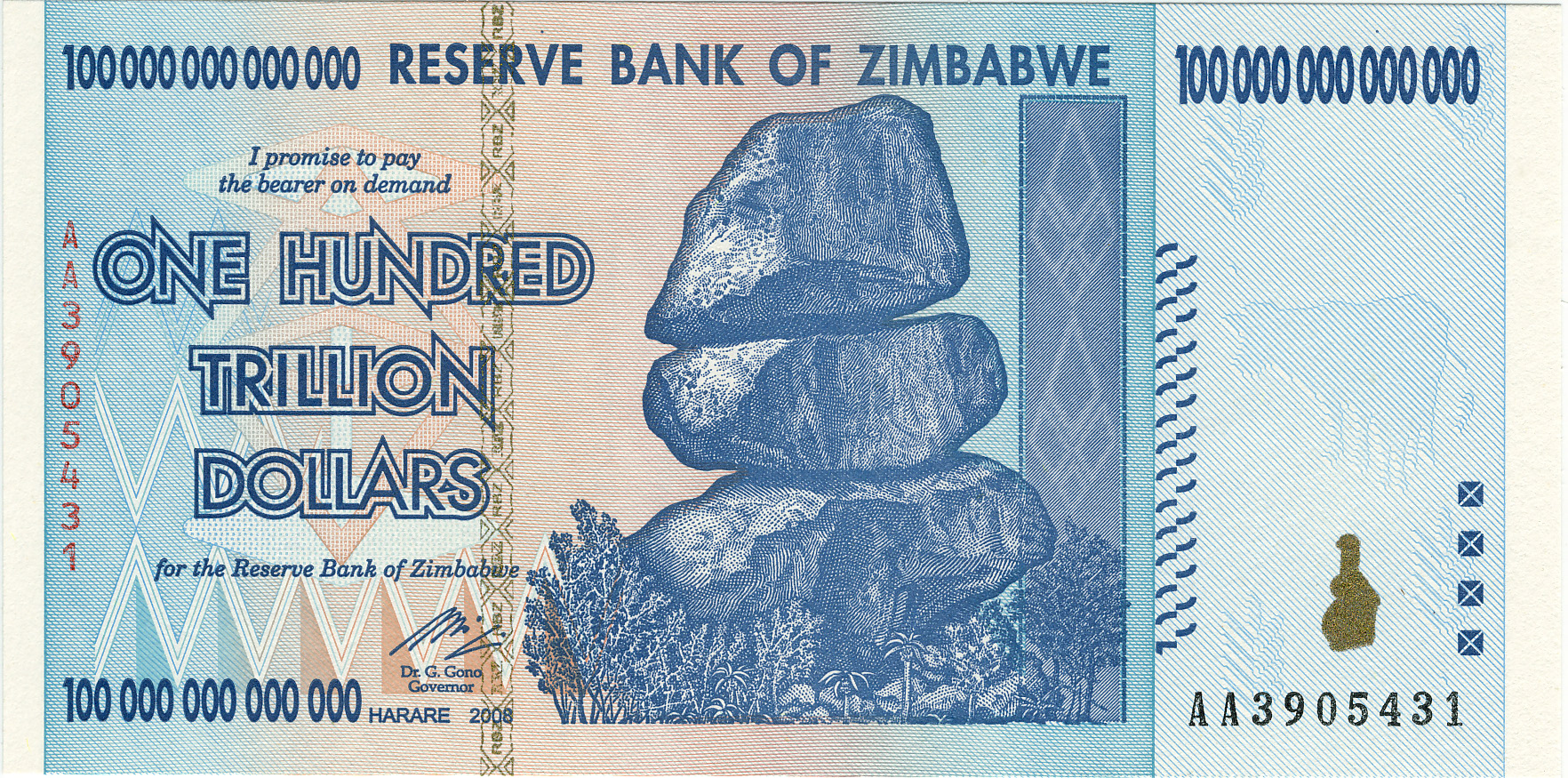

Focusing on the amount of coins you are mining or the coin supply is a joke. It's like praising Zimbabwe for producing 100T dollar notes, or the post WW1 Germany for having so much money you can build toy houses with them.

Market cap is deceptive

A lot of people rely on the market cap to determine which coin is the most valuable and worthwhile. Just have a look at CoinMarketCap. At the moment we have Bitcoin leading the market cap of about $10B, followed by Ripple at $1.2B.

Right at position number 2, we have an issue calculating the market cap - Ripple's available supply is listed at 35B XRP, although its total supply is shy of 100B XRP. If we calculated the market cap blindly, we should take the total supply and multiply it by the current price (0.0035 USD/XRP), which would net us $3.6B, rather than $1.2B.

The market cap is a poor metric for a coin with a highly-centralised supply. As Peter Todd jokingly put it - just mine a large amount of coins, sell a few of them at a high price and you've got a huge market cap.

It would be really hard to create some metric that can measure how valuable a cryptocurrency network is - market cap can be inflated, volume can be faked or hidden, you can't ever know how much of the coin supply is held by a handful of people with a million addresses, etc.

Inflation is not growth

In the past I've seen some deceptive advertising for a proof of stake coin that claimed it was a savings currency. They justified it by essentially saying - "buy our coin, then you can stake it and earn X% per year with it". While on surface it might appear so - if I start with 100 coins and at the end of the year I get 110 coins, then I'm 10 coins richer, right?

That works only on paper. If the market cap for the cryptocurrency remained unchanged and everyone got their 10% more coins, then you're right where you started - you own the exact same percentage of the economy as you used to. The inflation ate your earnings.

In economics, there is an important distinction between nominal and real interest rates. If I take a loan at 5% (nominal) interest rate, but the inflation is at 3%, then I effectively only pay a 2% (real) interest rate on the loan. Each year the principal of my loan has lower and lower purchasing power even if the number remains steady. The same is true for proof of stake inflationary coins - you're not earning anything with them, unless the pace of your earnings is faster than the overall inflation of the network.

A coin will only net you revenue if its equivalent of "real GDP" increases:

If you're not ahead, you're losing money

In an inflationary currency, if your supply of coins is growing slower than the average coin supply, you are essentially losing money. Earning 5% interest in a currency with 10% inflation means you are losing 5% on your investment in an ideal economy. In a real-life scenario, the markets would most likely be swayed a lot more by the speculation on the coin and whatever hype it can muster.

This point usually has low impact on most coins, but it seems to be exemplified with OneCoin's splits and tokens, assuming we would treat the coin as a real cryptocurrency and not a scam. In OneCoin, you can buy different packages that each come with a different amount of tokens and splits. If you buy the cheapest package for 110 EURO you get 1000 tokens and one split, but if you decide to spend 27'500 EURO, you get 300'000 tokens and three splits. This means that not only do you get about 20% discount on tokens when buying them in bulk, buy you can also split them more times (which I'm guessing would give you more mining tokens or something, I'm not sure). Because of this, if you're buying anything shy of the top-tier package, you're already falling behind. I guess that's why you can find a lot of "strategies" for buying the tokens everywhere...

Same goes for the doubling event, wherein everyone's coins got doubled (since 100% inflation equates to 100% growth or something...). If you missed that event, your purchases are only worth 50% of what they would've been before that event in proportion to the entire market. You can't ever catch up.

If you're late, you're paying the early adopters

Unless we're talking about cryptocurrencies with a flexible supply denominated in fiat, anyone adopting late is essentially paying the early adopters. In some cases, that's pretty justifiable - when Bitcoin was still fresh and nobody knew if it had staying power, you needed a lot of people to devote their time and energy into developing the infrastructure everyone relies on today.

This is why a lot of people in the crypto world despise premining and fast maturing coins - a few people hold a lot of coins and they get to reap the bulk of the money from anyone buying into the network. When the jig is up, they can cash out and it's the late adopters that get to hold the bags.

If OneCoin was an honest coin, I can see some people getting rich if and when the coin starts getting publicly traded and people can start dumping their coins. As it is now, it is likely that everyone with the coins will be holding the bags while the people behind the coin will be the one with the money.

Conclusions

Coin supply does not matter, market caps can be deceiving, nominal growth does not matter - only real growth, don't buy into scams.

Recently, the infamous OneCoin made news once more in the Bitcoin circles after their OneLife mastermind stream. One of the more interesting things mentioned was the previously announced blockchain reset, coin doubling and increase in coin generation speed. This is supposed to mean that OneCoin is getting more valuable, but once again, that's not how blockchain works - big numbers don't mean big money. But let's start from the beginning.

Bitcoin coin cap

As everyone knows by now, Bitcoin has a coin cap of around 21'000'000 coins. Each coin can be broken down into 100'000'000 satoshis, and that number can be further sub-divided in the future should the need arise. So for practical needs, Bitcoin has a final supply, and a nigh-infinite divisibility, as opposed to fiat currencies that are often nigh-infinite in supply, but finitely divisible.

The hidden genius of Bitcoin is very subtle when it comes to its coin cap and its precision that a lot of coin developers often miss entirely.

Sure, Bitcoin might not have a mathematically beautiful block reward (say, a power of 2 that halves every four years so that we can get a beautifully round number in the end), but it's still easy for programmers to work with. In financial computer science, precision is everything. A balance of $3.50 would not be represented in a database as a floating point number - those are imprecise. It would be an integer number, like 350 cents, or 35'000 hundredth of a cent if you need to get more precise. This makes sure that you can add, subtract and multiply those numbers all day long and you will always be right down to a penny.

Same goes for Bitcoin. Every transaction specifies exactly how many satoshis to transfer and to whom. The number is encoded in a 64 bit unsigned integer, meaning it can precisely express numbers between 0 and 2^64 (18'446'744'073'709'551'615). Even if you take all of the bitcoins that will ever exist and subdivide them into satoshis, you will get a number smaller than 2^51, meaning no matter how many coins you move back and forth, you will never lose precision or overflow the system. Moreover, the numbers can also be represented precisely with double-precision floating points (which has a precision of 2^52 for a fraction).

Other coins and their supply

Other coins have often toyed with different block reward schedules and thus different amount of coins.

Ripple is perhaps the most popular coin with a high coin supply, capping off at 100B XRP even. Their coins subdivide into 6 decimal places rather than 8 - this gives them an upper bound of under 2^57 units (if they instead went for 8 decimal places, they would be under 2^64 and wouldn't fit into signed integers). So they are fine in that regard, but they start to run into a problem when trying to express the units as floating points - they are only precise up to 2^52, or about 15 significant digits.

Same story with Dogecoin - currently sitting at 106B units with 8 decimal place precision, which is enough to start breaking the JSON API developers use. Bytecoin, sitting at 181B coins barely fits into 64 bit integers and FedoraCoin, the coin with the highest listed coin supply on CoinMarketCap breaks that limit with 438B coin supply, needing at least 66 bits to be fully represented.

When designing a cryptocurrency, there are many hidden pitfals one has to keep in mind and try to avoid. One might be tempted to create a currency with large numbers to give off an illusion of value where there is none. However, for practical reasons, you want to keep the numbers in your system within a reasonable range so the developers working with your coin won't have to deal with numbers too big to represent.

OneCoin might still be in the clear, at least as clear as Dogecoin is, but one more "blockchain restart" coupled with increased mining speed and they will be soon crossing the computer science boundary, at least assuming the system is legitimate to begin with.

Recently, I was contacted by a fellow Bitcoiner and informed about some possible shady goings-on on the DECENT platform. Reportedly, the platform has raised 5352BTC (3.2M USD equivalent) in its token presale, but the product appears to be on some shaky grounds. Lets have a look at what we can find out about the platform, the presale and have a look at whether there is something shady going on...

The Whitepaper

Any self-respecting blockchain project styles itself after Bitcoin and releases a whitepaper early on. Decent is no exception (#liberateyourself on every page...).

The paper starts with criticising Bitcoin for BOTH its low transaction throughput, and its large blocksize. Wouldn't it be nice if one could have a higher transaction throughput with a lower data footprint? Unless you start pruning old data, it won't happen. But that's apparently "some childhood diseases" Bitcoin has.

"Unfortunately, in spite of more than 6 years of its existence [Bitcoin] did not reach a position it could have attained mainly due to the imperfections in its architecture and design."

In comes Decent. Saving freedom of speech, solving the issue of authors having to figure out how to monetise their content, drive traffic to their sites, deal with Amazon's pay cut, etc. You can use it to publish "any text, picture, video or music content" (and even software) and "no third parties can control or influence the content".

The platform is characterised by being:

Independent - owned by the users and "will never be affiliated with any economic, media, or political party"

Borderless

Stable - not dependent on any single server

Fair - everyone starts at the same level and build up their reputation

Profitable - users can buy content directly from the authors and there is no cut taken by Decent

Spam Free - content publishing is expensive for spammers

Secure & Anonymous - authors can publish the content anonymously

Recommendations-enabled - readers that purchased the content can embed their feedback into the blockchain

While describing how the protocol works, we also learn that the application will be using the bittorent protocol with a distributed tracker to distribute its content. The torrent is downloaded by the "publishers" that charge a fee for storage and bandwidth. For encrypted content, the decryption keys are also distributed to the publishers.

Upon hearing what kind of content the platform will support, the cynic in me instantly reached two conclusions - a lot of the content, especially the movies and music, will be pirated like on current torrent websites, and a lot of the software content will contain malware. I somehow doubt I will be proven wrong...

So all in all, it looks like the system will use a blockchain to keep track of who paid for what content, while the actual content will be distributed over torrents. All in all, it looks like a poor man's version of MaidSafe or Storj, also somewhat similar to the Alexandria project. While those platforms focused on creating their own storage solutions paired with the blockchain, Decent appears to just mash Bitcoin and torrent technologies and produce something that's less than a sum of its parts.

A somewhat more usable solution would just focus on augmenting the torrent architecture without burdening it with a proprietary blockchain. You could use Factom or Ethereum to publish the magnet links, have some proof-of-payment solution to request the torrent data for paid content, or even just rely on donations from people that consume your content. Building one's own blockchain just to manage new tokens proves once again, a solution looking for a problem.

The token presale

Like a lot of projects in the crypto space, Decent is raising money through a token presale. To buy the tokens, you need to register an account on Decent's portal and pay bitcoins into a provided address. The tokens are distributed into the account and will later be available for withdrawal on the network proper. At the moment there doesn't appear to be an option of transferring the balance between accounts, so one is unlikely to be able to trade or sell the tokens before the network goes live.

Since it looks like Decent is handling all of the balances and not acting as a client-side wallet provider like Blockchain.info (that is, Decent probably handles all of the balances themselves), this can get really hairy for them from the regulators' perspective. Were they located in the USA, I would stay away from the service after what happened to Ripple Labs. Since the service does not seem to gather KYC information, it might be in a legal grey zone. Not being able to send the tokens around might actually be a benefit for the company - the token appears as a less of a security this way.

At any rate, the gathered bitcoins end up in 2-of-3 escrow with Coinbase. The three people responsible for handling the funds are:

Matej Michalko, the founder and director of Decent. Also, a co-founder of five different Bitcoin conferences (I suppose that is a new, fancy term for "organizer" nowadays), and a co-founder of two other crypto-related companies

Tibor Tarabek, reported to be the "Founder of Microsoft Slovakia", although his LinkedIn profile lists him only as a General Manager in years 1995-2000 (and also a "General Manager" of some "bitcoin, s.r.o." company between years 1992-1994, 16 years before Bitcoin was released!)

It is a bit strange that the founder of Decent is a co-signer of the escrow if you want to show that you can deliver on the project's promises. Find a few reputable Bitcoin people and use them for the entire escrow to show the release of funds is unbiased. Currently, all you need is one of the two extra people to co-conspire and you have full access to the 3.2M USD. While I might not know the reputation of mr Tarabek in the Slovakian Bitcoin space, his apparent lack of involvement with Bitcoin-related projects doesn't speak well to his ability to objectively judge a project like this.

All in all, I'm very dubious about how well the presale is handled. While it's not completely shady, I would not be surprised if the tokens get released before the project is finished or worse. To anyone that has purchased the tokens so far - hope for the best, prepare for the worst.

Matej Boda, who seems to be rather fresh out of university without much prior experience

Matej Michalko, the aforementioned co-founder of a lot of crypto-related projects. He appears to be business-focused

Wayman Kwan, a venture capitalist

So mostly business-focused founders. Let's look at the developers in the team:

Josef Sevcik, with background in Business Administration, Informatics and telecommunication

Bohdan Skriabin, a cryptographer still studying at a university

Lubos Novotný, an UX / designer

Stanislav Cherviakov, "a tech expert with a mathematical background" with experience in fintech, etc.

Vladimir Dubinin, a mathematician with a computer science degree

Anatoly Ressin, a programmer

And a lot of other advisers, ambassadors, etc. All in all, the development team is a bit mixed, having a few people that appear to have a lot of relevant experience, and some that are just starting out. The company also appears to be looking for a senior developer and a junior developer, both with a negotiable compensation payable in "other".

It looks like there are about 13 people making up the company proper. That can give the company a pretty high burn rate before any technical prototypes have been developed, but the costs may be rather low if the majority of the team is located in Slovakia.

Codebase

So far, Decent doesn't appear to be publicly owning up to any publicly available repositories on their website. However, the bitcoiner that prompted me to investigate the company pointed me in a direction of a github repository posted by Josef Sevcik, one of the developers on the Decent Team. It looks like a possible prototype of the Decent platform. The codebase appears to be based on Peershares with a small amount of changes (a few file diffs: 1, 2, 3).

Basing the codebase on proof-of-stakes based currency informs a lot of new things about the project that haven't really been mentioned on the project's website - the initial allocation of tokens (how much is being kept by the company and developers) can be really important when it comes to earning block rewards for example.

Conclusions

All in all, the Decent looks like an underwhelming solution looking for a problem. It is very unlikely the platform will solve all of the problems it sets out to fix - nobody will want to switch over to a new platform, use a new currency to get a glorified paywall. Focus on presaling the tokens doesn't seem to be improving the solution, as is often the case. Raising 3.2M USD before anyone has seen a prototype of the platform is similarly ludicrous. The tokens have little to no value during the presale - you can't trade them for speculation, you will only be able to use them once the platform launches, and there doesn't appear to be any special use for the tokens in the final system other than paying for things. I somehow doubt the platform will have 3.2M USD worth of content on it for years to come, so pre-purchasing a token now to be able to pay a movie for a few dollars or a blog article for a few cents a year down the line sounds like an awful proposition.

The escrow holing the coins doesn't appear to be following the industry's standards. It is not completely shady, but it could inspire more confidence.

The team behind the project looks fine - no "blockchain rockstar" stands out, but it seems to have everything needed. It is good that the company advertises its contact information, including physical addresses.

From the rumours I heard from a few fellow bitcoiners closer to the project, the company seems to be aggressively pushing for its presale with just a forked open source repo to back it up.

So in conclusion, the project doesn't look like it can live up to its own hype. The approach is rather naive, even if it can be fully realised. I see no reason to back it financially, and for anyone that has - I would like to know why? The token can't be traded, sold, speculated on until the project launches, which makes it a rather risky proposition.

Your post advocates a new:

(x) Altcoin

(x) Wallet

(x) Distributed data storage

Your idea will not work. Here is why it won't work.

(x) Your target audience is too small to support the project

(x) There is already a product on the market that does exactly what you’re doing, but ( ) faster / (x) cheaper / (x) better / (x) is more established / ( ) ______________

(x) Your project will not be compliant with the current (x) KYC / ( ) AML / ( ) gambling / (x) DMCA regulations

(x) Your solution is worse than general-purpose computing hardware / software

(x) Your presale tokens have no economic value

Specifically, your plan fails to account for:

(x) The existing regulations

(x) Public reluctance to accept weird new forms of money

(x) The known security exploits of the existing Internet services

(x) The human factor

(x) The problem of distinguishing between a human and a bot

and the following philosophical objections may also apply:

(x) Nobody likes DRM

(x) Ideas similar to yours are easy to come up with, yet none have ever been shown practical

(x) Feel-good measures do nothing to solve the problem

(x) I don’t trust YOU with the money

Furthermore, this is what I think about you:

(x) Sorry dude, but I don't think it would work.

Bitcoin Bullshit Tier

You are advertising a new Bitcoin / crypto related project. Based on the information provided, you have reached the Bullshit Tier of 3 for the following reasons:

Bitcoin Bullshit Tier 1 - marketing babble, technology misunderstanding

(x) “Blockchain”

(x) “As good as / better than Bitcoin”

Bitcoin Bullshit Tier 2 - willful misinformation, bait and switch

(x) Claiming your project can accomplish something hard without a clear explanation of how to do so

Bitcoin Bullshit Tier 3 - Many red flags

(x) Token IPO

Earlier this month, the G20 summit was held in China. One of the more interesting topics discussed, was the addition of Chinese yuan to the SDR - Special Drawing Rights. The topic of SDRs is rather important, but it doesn't seem to be discussed all that widely in the crypto community, so I figured I would cover it today.

Special Drawing Rights

Special Drawing Rights, or SDRs, are supplementary foreign exchange reserve assets defined and maintained by the International Monetary Fund (IMF). They were created in 1969. SDRs are allocated to countries by the IMF, and private parties do not hold or use them. The value of SDRs is based on a weighted basket of currencies (currently, 41% USD, 31% EUR, 11% CNY, 8% JPY and 8% GBP, worth about 1.39USD/SDR).

Special Drawing Rights are posed to replace the dollar as the world reserve currency. They serve well as a unit of account (due to lower volatility), can work well in international law (to have an objective measurement of value across multiple countries), and some countries even started pegging their currency to the SDR (due to increased transparency).

While the Special Drawing Rights are an interesting idea, they fall short in a one key area - they appear to be inaccessible for anyone short of a government. This can limit how useful the currency can be for say, creating international settlement, or using it as a measurement of value for corporations or even individuals.

If SDRs were a publicly available and tradable currency, it would be really interesting to see it used for pricing items, wages, etc. to counter currency wars. If your wage is pegged at 3000USD/month, whether USD goes up or down, you're paid the same amount of dollars. But if your wage was instead set at 3000SDR/month, you would receive the same value each month, no matter if it meant you got 2500USD when the dollar is strong, or 3500USD when it was weak. This could give anyone a protection from the government's meddling.

Crypto SDRs

Creating a currency based on a basket of other currencies is also not an entirely new idea in the crypto space either. Paul Grignon (author of Money as Debt) has described his take on the idea as Digital Coin back in 2009. A part of the system, called Perpetual Coin, would initially be issued based on a value of a basket of currencies. Unfortunately, the project never left the conceptual phase, and the website is down now, so it is unlikely we will see it ever implemented...

Other than that, there doesn't appear to be an SDR-pegged cryptocurrency out there. This might perhaps be due to the fact that we already have a better alternative to the Special Drawing Rights - Bitcoin. What it lacks in stable value at times, it more than makes up in terms of being all-inclusive and, at least so far, immune from government influence.

It wouldn't be hard, however, to create an SDR-Coin - it could function like Tether, or perhaps more accurately, like BitUSD since you couldn't exactly withdraw the coin. The main problem for a centralised issuer would be keeping the valuation of the currency stable, especially in periods where the basket of currencies is adjusted. Other than that, once the currency itself is created (and I would almost bet we would see someone make the currency after the article is published - 700+ cryptos is not enough after all), it would be interesting to see it start being used internationally. Perhaps we would finally see what is the real demand for SDRs for corporations and real people, rather than just governments. With any luck, this might just hurry the demise of the USD or "petrodollar" hegemony.

Conclusions

Special Drawing Rights are an interesting take on creating a new global reserve currency. While it is currently only accessible to governments, it could be very useful for corporations and end-users. For the time being, Bitcoin is the most accessible alternative for the rest of us.

DISCLAIMER: I work for Factom, which is mentioned in several examples in this article. While I work for Factom, the opinions expressed in this piece are, as always, my own.

Recently, I came across a token sale from the BlockSafe project. After a brief chat with the project's founder, I think this might be an interesting example of a blockchain solution looking for a problem and cashing in on some buzzwords. But let's start from the beginning...

Smart gun technology

A concept of a smart gun is nothing new - it's been around for at least 14 years. The premise is simple - it is a firearm that includes some technology only allowing for the gun to be used by an authorized user. It can be used to prevent "misuse, accidental shootings, gun thefts, use of the weapon against the owner, and self-harm". There are many approaches for user authentication - RFID chips, proximity tokens, fingerprints and biometrics, magnetic rings, mechanical locks, etc.

However, since most guns are inherently simple tools, and a lot of people would rather not have their defensive firearms "rely upon any technology more advanced than Newtonian physics" - batteries go dead, electronics malfunction, software bugs out, etc. Waiting for a blockchain transaction to confirm before your gun is unlocked is the last thing you want to be doing in a hurry.

Moreover, even if the technology was reliable, it would not be able to prevent every situation the society would want to avoid dealing with. Most gun deaths are suicides in the US, you wouldn't really be able to stop most mass shootings or other homicides without some major restrictions (like location-locking guns to one's home for example). Best it could do is restrict the use of stolen guns by people that wouldn't know how to crack or circumvent the DRM - a very small part of the issue.

The smarter the guns would become, the more concerns would be raised by people being paranoid the government would install a kill switch in their weapons to disable them remotely to "take away their freedom" and so on.

Lastly, it is very unlikely requiring any such technology would ever pass the NRA's lobbying in US's current political system. At very best it would be sold as an extra feature, but I somehow doubt there would be many end-user buyers for a gun with limited firing capabilities:

Blockchain for smart guns - good and bad ideas

There are many ways blockchains could be used in conjunction with smart guns, some more useful than the others. As the BlockSafe Foundation website (or their other, non-functional website, #gunsafety #liberty?) doesn't go into too much details on the specifics, let's explore a few options by ourselves.

Solution for the manufacturers - If the project is working up to manufacturer's spec, even if it was ultimately misinformed or using "the blockchain" as a buzzword, you can't really blame the developers for it. Even if using traditional solutions would've been better, they would be paid to deliver the solution in its current shape.

Data logging - If the gun would not be locked by the blockchain, but the solution was only used to log any discharges, or possibly even photos or other data, the blockchain might be used to ensure no data is lost or altered after the fact. This would be similar to how DHS uses Factom - to prove integrity of data. This approach would be especially useful for police and similar civil servants.

Ownership tracking - Instead of doing anything directly with the gun itself, the blockchain could be used to track the ownership of the guns themselves. This would work for both smart and traditional guns to establish an unalterable record of history if a firearm was to be used in a crime in the future. This would be a similar approach to Factom's land title record project. While this might be a good solution for the blockchain, it is very unlikely to pass through NRA as explained here.

Gun locks - possibly coupled with Ownership Tracking, the gun would essentially become a smart property. The gun would keep track of which private key owns it, and would only unlock itself if authorised by the proper private key - through RFID chip, smartphone app, etc. If the ownership would change, proper, new keys would be uploaded and so on. While it might sound like an interesting idea, allowing people to remotely disable their stolen property, etc., this approach would negatively effect the firearm's functionality as described in the previous section of the article.

All in all, it looks like most of the applications for blockchain-powered smart guns could basically be implemented in some straightforward smart contract on Ethereum or the like. Most of the complexity in the technology would come from everything that would be built on top of the blockchain. Now, with that in mind, let's look at how BlockSafe is selling itself...

Claims and buzzwords

Looking at BlockSafe's promotional video, we can list a number of claims, stated or implied, of what the project can do:

Prevent

Tragic amount of human suffering

Mass shootings

Unnecessary deadly force from police officers

Terrorist attacks

Gang violence

Citizens being killed by their own guns

Save lives

Secure one's firearms

Manage who can use their firearms

Locate and disable stolen weapons

Maintain a decentralised database

All powered by Trigger token. Other than the slew of buzzwords intended to appeal to emotions, it looks like the BlockSafe is designed to remotely control and track the guns. Looking at one of their infographics, the system also looks designed to be logging when the gun is used and notify emergency personel. This seems to be hitting on all of the major blockchain applications listed in the previous section, for better or worse.

Even if the project was to succeed, it is very unlikely it would accomplish all of its claims. A terrorist, a gang member, or a mass shooter would not choose a smart gun for their actions. You might get some chance of preventing people getting killed by someone taking their gun, but that's a slim percentage overall, about 0.02% of the gun owners would be killed by their own gun, which includes suicides. As for police officers using deadly force, it might have some dampening effect, but I somehow doubt it would make a significant impact if any.

So what would the Trigger token be likely used for? Well, if you would pay to place logs of the gun into the blockchain, then that's defeating the point - you want every log to go into the chain and not allow people to withdraw their funds to prevent logs from happening. You would need some sort of transactional currency for that, or a centralised solution maintained and paid for by the manufacturer (in which case, you don't need much of a blockchain). Using triggers to transfer gun ownership might be possible, but it might not occur often enough to maintain the network. Using the tokens to unlock the gun would be outright malicious.

Conclusions

All in all, the BlockSafe project looks like a solution looking for a problem and wanting to use a public blockchain to boot. The token presale looks like pure speculation - the project itself doesn't look like it needs the tokens, nor is there a clear explanation of what the tokens would be used for.

The smart gun technology as hinted by their video doesn't look useful. While that might not matter if the project already has industry partners committed to using the project, it might be an important thing to keep in mind for the token speculators - if nobody wants to use the technology, the tokens will ultimately be worthless. If the industry partners are paying for the technology, why sell the tokens at all?

All in all, most of the goals smart guns wish to accomplish could be accomplished easier with a physical lock on the gun, or putting the gun in a safe.

Ultimately, if you are focused on saving lives and reducing gun-related deaths, ban the guns like Australia did, don't run a token presale for some blockchain project...

Your post advocates a new:

(x) Altcoin

(x) Permissioned blockchain

Your idea will not work. Here is why it won't work.

(x) Your target audience is too small to support the project

(x) The proposed security model is (x) flawed / ( ) not enough / ( ) completely wrong and therefore you will be ( ) scammed / ( ) hacked / ( ) stolen from / (x) circumvented quickly

(x) There is already a product on the market that does exactly what you’re doing, but (x) faster / (x) cheaper / (x) better / ( ) is more established / ( ) ______________

(x) You rely on proprietary (x) hardware / (x) software / ( ) intellectual property / ( ) _________

(x) The solution would work better as a (x) centralised / (x) decentralised / ( ) distributed solution

(x) Your solution is worse than general-purpose computing hardware / software

(x) Your solution will make the current hardware / software perform significantly worse

(x) Your presale tokens have no economic value

Specifically, your plan fails to account for:

(x) Public reluctance to accept weird new forms of money

(x) The human factor

(x) The problems computers have with interacting with the real world

(x) Strong lobby groups opposed to solutions like yours

and the following philosophical objections may also apply:

(x) Nobody likes DRM

(x) Ideas similar to yours are easy to come up with, yet none have ever been shown practical

(x) Whitelists suck

(x) Feel-good measures do nothing to solve the problem

Furthermore, this is what I think about you:

(x) Sorry dude, but I don't think it would work.

Bitcoin Bullshit Tier

You are advertising a new Bitcoin / crypto related project. Based on the information provided, you have reached the Bullshit Tier of 3 for the following reasons:

Bitcoin Bullshit Tier 2 - willful misinformation, bait and switch

(x) Claiming your project can accomplish something hard without a clear explanation of how to do so

Bitcoin Bullshit Tier 3 - Many red flags

(x) Token IPO

(x) Logical fallacy: ( ) false equivalence / ( ) false dichotomy / (x) appeal to emotion

(x) Providing no company contact information

As discussed last week, Bitfinex has followed through with their bail-in and gave all of their users a 36% "haircut". While not ideal, with the right approach and conviction, this might be a way for the exchange to eventually right their customers. The idea is not new - I recall discussing something similar a few years ago when another big exchange was not measuring up...

MtGox's secondary market

MtGox, the poster child of why one shouldn't trust exchanges with one's BTC, has officially shut down in 2014. However, months before that you could already see some red flags popping up that something was going wrong. MtGox started having some fiat withdrawal problems, and as a result, its market was off by 10+% and ripe for arbitrage. Some people could make a tidy profit churning money around, provided they could get their fiat out of the exchange.

A few months later, the situation got worse - MtGox has officially halted both its bitcoin and fiat withdrawals altogether. However, probably due to some interesting code optimisation, someone figured out that if you withdraw bitcoins straight into a deposit address of another MtGox account, the funds would be transferred without creating a transaction on the blockchain. It looked like that functionality was governed by the "MOVE" API call, rather than "SEND". This tiny functionality was enough for someone to build an entire secondary market for MtGox before the whole exchange went under.

While I can't find any reference to what the site was (EDIT: the website was Bitcoin Builder, as pointed out by /u/samurai321), as the news of MtGox collapse has probably buried it in the sands of time, I remember it being a simple BTC-MtGoxBTC exchange. One could deposit actual bitcoins and trade them for bitcoins owed by MtGox that were moved to the secondary market's address. It allowed some people to get rid of their coins frozen at the exchange and cash out to the safety of the wallets their own, while letting others speculate on whether or not MtGox would be going under. I remember seeing the price reaching a level of 30+% discount on the market, which is fairly comparable to the current Bitfinex scenario...

Decentralised secondary markets

After MtGox collapsed, I haven't seen a similar secondary market pop up anywhere. The closest thing that comes to mind is being able to trade Bitstamp's IOUs on Ripple, which might be an ideal approach for trading exchanges' debt (at least provided the exchange doesn't run into new hacks). If Bitstamp was to go under, you could still trade about 1.5M USD and 2k BTC of its issue on the decentralised exchange nearly indefinitely. Figuring out its USD-USD and BTC-BTC exchange rate against an operating pool could be a clear gaige of confidence in the platform - if there were talks of the exchange recovering, the price might get closer to parity, or go away from it in the opposite case.

At the same time, such a secondary market might be used for something more morally muddy...

Buying one's own debt

Say Bitfinex's tokens were tradable during the hack. Before everyone knew how much was lost percentage-wise, the market would be wild with speculation - you probably could buy bitcoins at 50+% discount, perhaps even at 90% discount if the fear would set in. Now, if Bitfinex was aware of such a situation and knew how much deposits they could actually cover, they could try buying up their own debt for pennies on the dollar before the haircut was to take place. This could allow them to buy off some of their debt at a discount, reducing their obligations to their customers and therefore creating a theoretical profit.

Such a scenario would be highly unethical and I would guess highly illegal, but I wouldn't be surprised to see something like this happen sooner or later in the Bitcoin world. Instead, let's imagine some more ethical approach Bitfinex could act on their current situation...

Slow debt repayment

I'm not sure how Bitfinex structured their token program as I don't use the exchange. However, a good approach to eventually righting everyone would be for them to convert everyone's BTC balance into those tokens. At any time, the users would be able to cash the tokens in and get actual coins, minus the haircut. With each token converted, their obligations would decrease.

The tokens would also be tradable on the exchange itself for actual coins, creating a market for the debt. Anyone wishing to speculate would be able to trade the coins for a value between the haircut discount and 1BTC. The price would have upper and lower bounds, but could fluctuate in between.

If Bitfinex was diligent and set on repaying the debt by eventually buying up all of the tokens, they could publicly declare their strategy of doing so - perhaps a portion of their monthly income would go directly into purchasing the tokens from the market at the spot rate. With every purchase, the amount of tokens in circulation would decrease, thus the ratio of their bitcoins earmarked for buying back the tokens to the actual amount of tokens would increase, making the haircut smaller and smaller. Gradually, the gap between the value of the tokens and the real coins would shrink so much they could convert the tokens themselves straight into coins at a 1:1 ratio and remove them entirely.

In the end, the amount of coins you would get back would rely only on how quickly you need them - you could get them today for 36% off, perhaps get them for 30% off in a year, or get a full amount in a decade. The market would decide what the future value of the tokens would be, and with each month (and perhaps with each trade if some fees were to be maintained for this market), the debt would be slowly repaid.

In the end, this is an optimistic scenario assuming the exchange could earn back millions of dollars worth of coins before the company would go under. Similarly, if you believe the value of bitcoins will go up, the debt may never be repaid - the value of the coins left to be repaid could be going up as the number of the coins would be going down thanks to the increasing price.

One way or the other, it would be a really interesting case study if Bitfinex was to implement something like this...

This week, a high-profile Bitcoin theft took place at the Bitfinex exchange. The attacker reportedly stole 119'756BTC, worth about 70.5M USD. Those funds were held at a 2-out-of-3 multisignature wallet - one key was held at Bitfinex's server, another was kept by BitGo, and a third was a backup key held offline by Bitfinex. From what the reports say, the hacker was able to get their hands on the first key, as well as the API credentials required to authorise BitGo to process the withdrawal. With no additional safeguards, they were able to drain the hot wallet and land themselves around the number 2 spot of the biggest Bitcoin theft to date, after MtGox.

The scenario is still unfolding, so there are a lot of theories still floating around as to why the situation was allowed to take place. Some have speculated Bitfinex was forced to keep all of their coins in a hot wallet due to CFTC's ruling (as Bitfinex was not a registered futures trading platform), although it seems that the change was made before the ruling. Bitfinex also unveiled a plan for a "bail in", wherein everyone's assets would be devalued by about 36% so the exchange could continue operating.

Since Bitcoin's past seems to be littered with theft, I would like to have a look at one possible solution to minimise such high-profile hacks:

The way Voting Pools help secure users' funds is through shared responsibility from competing actors. Multiple exchanges of similar size would group together in a pool and secure one another's funds through multisig and a legal agreement to share responsibility in an event of a loss (be it from theft or one of the exchanges trying to run off with everyone's money). The multisig would be distributed in such a way that any one actor would not be able to control even their own money, and the system being robust enough to handle a loss of some keys (2-of-3, 3-of-5, 4-of-5, etc.).

This setup would make sure that a critical failure of one actor would not compromise the system. Even if one of the exchanges would burn down, get hacked, or the owner would decide to run away with all of the private keys, they couldn't do anything. The other exchanges would take over the responsibility and secure all of the funds to be able to pay all of the failed exchange's customers without suffering a loss of their own funds.

More importantly, however, this solution also forces every participating company to not only police themselves and ensure they have the most adequate security practices in place, but also to look at one another. When your own money is on the line, you will make sure everyone is keeping up with the rest of the pack in terms of keeping the money safe. Since the exchanges would still be competing with one another, they would have every incentive to expose other actors in the voting pool that are compromising the security.

Beyond that the full implementation of Voting Pools also necessitate that the exchanges would open up their transaction logs to one another to make sure everyone knows how much every customer is owed in case of a database wipe or the exchange vanishing from the face of the earth. This is pretty much automatic when it comes to gateways on a public ledger like Ripple or some shared permissioned blockchain, and it shouldn't be too hard to accomplish if an exchange already creates a strict and timely Proof of Solvency. That being said, it is pretty much unheard of for a normal Bitcoin exchange to do that currently, which might make it more problematic.

Having access to a full, real-time set of transaction logs the participants in a voting pool have everything they need to not only be able to settle with every customer in case the exchange goes under, but they can also police the exchange in real-time and raise flags in case of discrepancy. If exchange's liabilities exceed their assets, all withdrawals can be automatically haled until the matter is resolved. Large withdrawals, sudden market crashes and balance changes could similarly raise a lot of flags (to avoid another MtGox scenario, wherein a hacker crashed the market to be able to bypass the $1000/day withdraw limit).

Conclusions

All in all, voting pools would force a strong degree of transparency on every actor and couple that with multiple security teams making sure the system is secured against a growing number of hacks. While the participating exchanges would sacrifice their business data secrecy to their direct competitors, security through obscurity is never a good approach.

Leaving aside the discussion as to which approach would be the best for Bitcoin in the long run, we can agree that there is a disagreement on the issue and any hard fork that may happen will not be as unanimous as the previous forks were. Looking at some recent examples, we can expect that any contentious Bitcoin fork will create a split in the network.

Big players can trump forks - Elacoin

Last year Steve Sokolowski shared his thoughts on a Bitcoin hard fork proposal in a forum post. Other than discussing the actual solution, Steve also shared a story of Elacoin's attempted hard fork. Apparently, it was some unremarkable Proof of Work altcoin which activity has died off after awhile. A new developer came in and decided to breathe new life into the coin by creating a Proof-of-Stake fork. A lot of people got excited for the update and the trading volume and price rose back up.

When the fork was scheduled to take place, despite the backing of the community, the developers and stakers, the fork failed since Cryptsy continued to trade the coin without upgrading their daemon. Eventually the hard fork was deemed a failure while the old coins were still being traded.

This brings to mind the famous experiments with five monkeys, a ladder and a banana. People would trade a coin in anticipation of the fork, then ignore the fork and continue trading the coin due to its increased price and volume, completely forgetting why they were trading it in the first place. Classical altcoin speculators.

This only goes to show that big players, even if they are in a minority, can trump developer forks. While a story like this is rather unlikely to happen in Bitcoin, since the coin itself has many different markets and a vast community, we could experience a different problem when a hard fork happens...

New Coke vs Coke Classic - Ethereum

Not so long ago, Ethereum has experienced The DAO debacle, wherein a large quantity of ethers were drained from a high-profile smart contract. This prompted the Ethereum developers to create a hard fork that invalidated the attack. For a few days everything seemed to go smoothly - the majority of the network supported the fork, everyone transitioned just fine and it looked like the network could put the kerfuffle behind them. Then came Ethereum Classic...

Ethereum Classic is, I suppose, an "un-fork" of Ethereum - a codebase designed to ignore the DAO hard fork and continue the network as if it never happened. Whether the developers believe that they are supporting the community that disagrees with the fork, or they just want to make a quick buck, the fact is that the classic ethers (ETC) started being traded on Poloniex, probably one of the biggest altcoin exchanges currently, and now are being actively traded on a number of other exchanges with a current market cap of $200M and 24h trade volume of $65k - forth market cap after Bitcoin, Ethereum and Ripple, and having double the trading volume of Ethereum, second only to Bitcoin...

From a perspective of any Bitcoin core developer wanting to fork Bitcoin, this is probably the worst thing that could have happened in the given situation. Exchanges supporting both sides of a fork can set a precedent of what will happen when Bitcoin is forked in any fashion short of full unanimity. Even if the unforked version of Bitcoin has 1% of its market cap, that's $94M market waiting for an exchange to take their money - it would be the 7th largest coin market, around the halfway point between Litecoin and Dash.

As an Ethereum Developer pointed out in an Ethereum Foundation Skype Chat leak - ignoring Ethereum Classic means there is no money to be made, while embracing it allows you to tap into some "vestigial value remaining from the shared chain history".

Even if any potential fork has all of the support from all of the developers and miners, there isn't much one can do to stop the un-fork, perhaps short of a Coiledcoin-esque 51% attack. Even if networks like Ethereum implemented "the bomb" (a special smart contract that prints tokens out of thin air, intended to kill an un-forked network), a developer could just create another hard fork to disable that code pretty much like the DAO was disabled...

Kill it with fire

So when all is said and done, it looks like the only way to ensure only one version of Bitcoin is around, one would need to reach an overwhelming consensus with the developers, the miners and the exchanges to support only one part of the fork. Anything short of that will create a split network with duplicate tokens being created on both tines of the fork.

To ensure the rest of the network follows suit, someone should put aside some funds and mining power to be able to execute 51% attacks on any un-fork that would start being traded at an exchange. While a 51% attack in normal cases might be in the legal murky territory, perhaps using it to enforce a hard fork might not be seen as an attack on the currency, but as a part of the upgrade process. The law might not catch up to this conundrum for years still.

Conclusions

Anything short of an unanimous hard fork to Bitcoin will most likely result in a network split where both sides of the fork. The split will most likely be motivated by short-term profit to extract some remaining value from the alt-chain. A good way to ensure no such split happens would be to divert some resources to performing 51% attacks on the minority chain and thus causing whatever exchange that tries to trade them to lose money.

In the recent weeks there has been a resurgence of news about OneCoin, what appears to be a high-profile MLM ponzi scheme disguised as an altcoin. From what I can gather, the renewed popularity of the topic was sparked by OneCoin's Coin Rush Global Event:

Coin Rush Global Event

Watching this video as someone that has been around Bitcoin for 5 years now, there are more red flags here than you would see during International Workers' Day in some places. In fact, the video and OneCoin in general are such a good example of how you can bamboozle people by saying just the right thing that it might be a worthwhile exercise to dissect a lot of it.

The Basics

Going onto a cryptocurrency website you want to look for a few key pieces of information:

Who is developing the project / the code? You want to find at least a competent development team identifying themselves. Examples: Bitcoin, Ethereum, Ripple. For OneCoin, the best resource I could come across was OneDream Team's "Top Leaders", which only boasts some news.

Where is the company located? It is especially important for exchanges and other companies you're giving money to, but can be useful for the core development team if applicable. Examples: Ethereum (listed on the bottom page), Bitcoin Foundation, BitStamp, not as much for Bitcoin Core (as it's a more decentralised development) Ripple, OneCoin or xcoinx.

Where is the source code? If you can't see the code, you can't be sure what you're installing isn't malware or whether the blockchain itself is really there. Examples: Bitcoin, Ethereum, Ripple, but nothing for OneCoin.

Do any reputable exchanges trade it? A coin that isn't tradeable might not be a currency at all, but instead some "funny money". For a smorgasbord of examples, you can check out CoinMarketCap, indexing things as low as $8 market cap for COIN. OneCoin, despite boasting 5.2B USD market cap, is conspicuously missing...

Getting all five of the above points is a good start for any currency, but as we can see, even some of the largest coins are missing one or two of those features. Lacking all five does not bode well.

That's not how blockchain works

Putting all of that aside, let's look at the video proper and see what the event is about. Apparently the big news that day was that OneCoin is retiring it's old blockchain (!) and launching a new one in October so they can make more onecoins (!!). The justification being, and I kid you not, that they need more coins to grow, since there might not be enough coins for new merchants, Latin America, India, etc.

Let that sink in for a bit. A cryptocurrency that is not explicitly tied to a fiat currency is running out of coins for people. So instead of letting free market organically settle on a price it thinks the coins are worth and say, buying the coins from the market to give to the new merchants if they want, they instead decide to make more coins...

The issue is also more complicated than just that. OneCoin on its FAQ page claims its blockchain is mined with a custom solution based on Script and X11. However, you don't mine the blocks directly, instead "you just sign up on the mining dashboard on the exchange in your back office". This might remind some people of Proof of Stake or Delegated Proof of Stake, but no, OneCoin does it differently - "People are signed up and assigned to mining pools on a first come, first serve basis. Whenever a place is free you can join a pool.". The process appears to be:

You send OneCoin money to buy the right to mine the coin

You sign up to mine

You wait for your turn to mine

You get your coins

In other words, it's like purchasing coins from an exchange (send money, get coins), but with an arbitrary wait period (currently 3-6 MONTHS!) between sending money and receiving coins. As /u/TimTayshun pointed out, the block times are also very strange - too regular for a Bitcoin-like mining scheme. The blocks appear to be generated at the 10 minute mark without much variation. If there is any real mining going on, there is no real competition, no difficulty adjustment or anything like that. It looks a lot more like Ripple's Consensus algorithm than anything mining-related.

Splits and tokens

But even all of that is not the whole story. Enter the splits and tokens. You don't directly buy the onecoins, instead you buy packages that include tokens and splits:

Apparently in order to keep the price attractive, you split the tokens as you would company shares. In the end it means that you have a higher quantity of tokens that you can use for mining, but the value stays the same, I think. The splits apparently can only be used on the tokens, not the coins that are mined, and you can combo the various packages in some "strategy" to receive more and more splits.

This seems to accomplish a few things:

Make the process more opaque

Incentivise people to buy more and more packages to get the best value for their money

Make people feel like they are in control of how to get the most money and get ahead of everyone else

Widen the distance between real money and onecoins by extra few steps in a freemium-like model

So in other words, the entire system looks like a shady mobile app:

Because nothing inspires more confidence than a pyramid-like structure with the money flowing to the top...

There is also something about not actually purchasing tokens, but instead purchasing training from OneAcademy that conveniently comes with tokens, BVs and what have you, but at this point I think I made my point. Purchasing any cryptocurrency is simple - you take your money, you get your tokens. With OneCoin, a simple trade is a drawn out process taking many months with zero transparency. Mining is a joke, the numbers are multiplied over and over. But the story doesn't end there...

Show us your proof

During the Coin Rush Global Event, there have been a number of claims made about OneCoin and other coins as well. After hearing a lot of them, one feels the urge to shout "show us your proof". In no particular order:

OneCoin has 2 million active users, no other currency has as much - I would love to see a proof of that claim, since it not only asserts a lot of people are using OneCoin, but claims to know how many people are using other cryptocurrencies, which is an information that is hard to come by. Someone estimated Bitcoin to have 50M users by 2015, but that's a guess. How many people are actually active on Bitcoin or OneCoin, that would be interesting to know.

OneCoin has 4.5B USD market cap - seeing as the coins aren't actively traded at any reputable exchange and the blockchain is not verifiable, any number you throw out there is as valid as any other.

Bitcoin has almost no merchants taking it - there are 8000 physical locations taking Bitcoin today, in 2014 BitPay estimated the number to be over 20k. All in all, it would be interesting to see where the data is coming from, since it's not that easy to come by

OneCoin is in 195 countries, it's bigger than Western Union - It would be really interesting to see the actual list of their operations. There are 195 countries in the world, which means they would have to operate in the US, North Korea, Iran Sudan, Syria and Myanmar at the same time, violating a lot of international sanctions.

OneCoin can do more transactions than Visa and Mastercard combined - this would mean it can handle more than 2'000 transactions per second, it would be an impressive amount of data to synchronise in a blockchain

OneCoin stores all customer KYC information encrypted on the blockchain - this would not only be a huge customer data protection concern (blockchain by definition is shared between multiple parties, so all you need is a blockchain and encryption key leak and someone has compromised all of that data), but also an can be an issue of how decryption would be handled under a warrant

Even after pointing out the various problems for a long while, there is still a lot more that needs to be addressed. Going into detail on everything would probably make this lengthy article probably twice as long. So let's finish off everything else in some quicker fashion. What follows are various claims, quotes and other titbits from the video presentation:

It takes over a year to mine one bitcoin - unless you're 21.co, nobody advocates Bitcoin mining to newcomers. Just like mining gold in real life, it's best left to professional companies

There are "Mickey Mouse coins" that copy OneCoin's concept - don't flatter yourself, everyone is aping Bitcoin

Just like you need a driver's license to drive a car, you need a drivers license for the cryptocurrencies - one of the beautiful things about Bitcoin is that it's inclusive - anyone can use it, you don't need a permission. While education is valuable, forcing people to go through a test before they can use cryptos is missing the point

OneCoin wants to be number 1 cryptocurrency world-wide in 2 years

When Bitcoin was one year old, it was worth 15 cents and nobody cared about it - it took two years for Bitcoin to be worth 15 cents, but now the speed at which good coins accelerate in price has increased thanks to Bitcoin. Dissing on the history to make your coin appear better is a false equivalence

OneCoin is one year old and it already wrote history - not really, but it will certainly write history once the jig will be up

They are aiming to have 20 million active users and 1 million merchants in 2 years

"We are the bigger community - we decide what the philosophy of cryptocurrency is"

The merchant / Latin America / India market capitalization is X trillions, OneCoin is only worth 5 billion, it simply does not work - normal coin would allow the price to grow to accommodate the market and use the 8 decimal places the coin has. Saying that you need to increase the amount of coins to grow is like saying you need to slice an apple into more pieces to make it bigger

"We can close new registrations, reject merchants... Or make more coins!"

"Biggest coin out there is Ripplecoin [sic], with 100 billion coins[sic]", and OneCoin will increase its number of coins to 120 Billion to be bigger than Ripple - that will still make you 3 times smaller than Fedoracoin, why not go for more?

You can't increase the amount with the current blockchain, need to retire the blockchain and launch a "new, more powerful blockchain" - you could, if your developers were up to snuff. Or maybe you're doing this to delete some old data from the old blockchain, or introduce some different balances that aren't supposed to be there?

Every account balance will be doubled after the blockchain is updated - again, increasing the numbers is not the same as increasing the value those numbers represent

When posting a question "will my coins be worth less after the update", the answer is not a clear "yes or no", but instead saying that the value of coins comes from brand and usability

Restaurant or retail store will never take Bitcoin - 8000 times false

"OneCoin will write history, and the cryptocurrency comminuty will have to rewrite philosophy"

OneCoin, officially based in Dubai, boasts an impressive "ecosystem", consisting of 10 distinct items:

OneCoin's ecosystem

OneAcademy, an e-learning platform teaching about tarding, stock exchange, cryptocurrency, etc. in a 6-level program, boasting over 2'000'000 students and supporting 231 out of the current 195 world countries

OneExchange, currently not online

OneLife Network - "a digital platform with a unique ecosystem of sophisticated products and social networking tools that help members achieve financial independence", whatever that's supposed to mean. But fret not, they will offer you an "Ultimate Trader Package" for the low low price of 118'000 EUR, and a tablet to match for 550EUR, only 5-6 times more expensive than a comparable tablet. No contact information

CoinCloud - a cloud storage where you can buy 100GB of data space for 1 year for 3'030 EUR, which is about 1'500 times more expensive than Google Drive

There are 195-206 countries in the world. OneAcademy supports 231 of them

Conclusions

OneCoin, perhaps going in Microsoft's footsteps of wishing their products to be abbreviated into "The One" has raised a lot of red flags on all fronts. It does not instil any confidence in its products, its business strategy, or legitimacy of its creators. It takes money from a lot of people, turns it into a flashy show to boost confidence, and talks about its "community" and "family". The way it does business is overly complicated, intentionally opaque, and unverifiable. It is a blockchain and cryptocurrency only by self-proclamation. Keep as far away as you can from anything related and enjoy the slow-motion train wreck.

Your post advocates a new:

(x) Altcoin

(x) Permissioned blockchain

(x) Centralised / decentralised exchange

(x) Remittance service

(x) Gambling website

(x) Investment scheme

(x) Wallet

(x) Mining service (hardware, software, etc.)

(x) Mining pool

Your idea will not work. Here is why it won't work.

(x) The proposed security model is (x) flawed / ( ) not enough / (x) completely wrong and therefore you will be ( ) scammed / ( ) hacked / ( ) stolen from / (x) implode quickly

(x) There is already a product on the market that does exactly what you’re doing, but (x) faster / (x) cheaper / (x) better / (x) is more established / (x) is not a scam

(x) You are proposing exorbitant fees for the use of your product that are unsustainable in the long run

(x) Your product gives unfair preferential treatment to (x) yourself / (x) the earliest adopters / ( ) early investors / ( ) select few / ( ) _____________________

(x) You violate the core principles of Bitcoin, including: (x) core cryptography of the protocol / ( ) 21M coin limit / ( ) coin distribution / (x) ownership of private keys / (x) inclusive nature of the network / (x) pseudonymity of users / (x) lack of transaction censorship / ( ) ______________

(x) You promise unreasonable return on investment without a clear business model of where the money is coming from

(x) Your project cannot be run legally at your jurisdiction

(x) Your project will not be compliant with the current ( ) KYC / ( ) AML / (x) gambling / (x) MLM regulations

(x) You rely on proprietary ( ) hardware / (x) software / ( ) intellectual property / ( ) _________

x) Your solution is worse than general-purpose computing hardware / software

(x) Your product is poorly implemented

(x) Your presale tokens have no economic value

(x) Your adoption goals are unrealistic

(x) Your product has zero transparency

Specifically, your plan fails to account for:

(x) The existing regulations

(x) The required Money Services Business license

(x) The anonymous nature of cryptography

(x) The geopolitical map of the world

(x) Adaptability to growth of the market cap

(x) The miner incentives

(x) Public reluctance to accept weird new forms of money

(x) Huge existing software and hardware investment in Bitcoin

(x) The known security exploits of the existing Internet services

(x) Secrecy of data decryption

(x) Increase in currency unit supply not being the same thing as increase in wealth

(x) Disproportionate increase in currency units drains wealth from one group into another

(x) The long-term sustainability of the project

and the following philosophical objections may also apply:

(x) It is a MLM scam

(x) It is a pump and dump

(x) It is a (x) ponzi / (x) pyramid / ( ) ___________ scheme

(x) A known (x) scammer / (x) person with poor reputation is involved with your project

(x) Why should we have to trust you and your servers?

(x) Incompatibility with open source or open source licenses

(x) Feel-good measures do nothing to solve the problem

(x) Extraordinary claims require extraordinary evidence (aka “Proof or GTFO”)

(x) I don’t trust YOU with the money

Furthermore, this is what I think about you:

(x) Sorry dude, but I don't think it would work.

(x) This is a stupid idea, and you're a stupid person for suggesting it.

(x) You’re a scammer and you should feel bad.

Bitcoin Bullshit Tier

You are advertising a new Bitcoin / crypto related project. Based on the information provided, you have reached the Bullshit Tier of 4 for the following reasons:

Bitcoin Bullshit Tier 1 - marketing babble, technology misunderstanding

(x) “Blockchain”

(x) “As good as / better than Bitcoin”

(x) Misunderstanding the technology

Bitcoin Bullshit Tier 2 - willful misinformation, bait and switch

(x) Selling overpriced / underperforming hardware or software

(x) Claiming your project can accomplish something hard without a clear explanation of how to do so

Bitcoin Bullshit Tier 3 - Many red flags

(x) Assuring your product is legal

(x) Speaking about profits / return on investment

(x) Providing no company contact information

(x) Multiplying coins

(x) Rebooting the blockchain

(x) Company being hosted in hard to reach countries

(x) Claiming your product services / is available at a large amount of institutions without a proof

Bitcoin Bullshit Tier 4 - Outright scams

(x) High return on investment

(x) Describing a financial security and claiming it’s not a security

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}